This booklet is presented on behalf of the many Americans who sincerely want to be free … and the many more who think they are.

Many thanks to those dedicated individuals who have ceaselessly given of themselves to arouse an unsuspecting public as to the grave social and economic consequences we face, with special thanks to the Monetary Realists who have preserved the essence of the late Merrill Jenkins.

It is my sincere and fervent hope the reader will sense the magnitude of our plight and the urgency required to effect its resolution. May God grant you the wisdom to see and the strength to endure, for the time draws near when you must choose the path you will follow and let your ways be established.

In tendering the necessary Federal Reserve Notes to make this booklet possible, I hereby acknowledge the following:

- Federal Reserve Notes are

liabilities

of the Federal Reserve Bank … a private corporation. - Federal Reserve Notes are non-redeemable … our monetary authority thereby acknowledging bankruptcy.

- These FED Notes are evidence of

monetized debt,

being I.O.U./U.O.Me negotiable instruments. - Liabilities cannot pay off a debt … thereby leaving this transaction incomplete; the publisher having not been paid for this publication. I have merely transferred evidence of debt that cannot be paid.

- I therefore disclaim all responsibility for my part in this monetary hoax, despite my awareness.

Money is a subject we all take a superficial interest in, but seldom do we seek an understanding of its nature or the consequences of leaving such matters to our experts.

If we were to think diligently about such terms as money, dollar, credit, bonds,

etc. we might just realize we have let familiarity breed contempt, just as many of us have come to take for granted such things as telephones, televisions, airplanes and the internal combustion engine. But how many of us fully understand how these things work, despite their everyday use? Keeping this in mind, let us examine more closely this thing called money

and perhaps lay bare the reason for our distressed economy.

All the perplexities, confusions and distresses in America arise not from defects in the Constitution or confederation, not from want of honor or virtue, as much as from downright ignorance of the nature of coin, credit and circulation!

John Adams

Webster’s Collegiate Dictionary defines money as:

1. Metal, as gold, silver or copper, coined or stamped, and issued as a medium of exchange. Also … Anything customarily used as a medium of exchange and measure of value, as sheep, wampum, gold dust, etc.

6. Written or stamped promises or certificates, which pass current as a means of payment.

Funk & Wagnalls Standard Desk Dictionary adds a further definition of money

:

4. Money of account.

Most people would agree that money means: a medium of exchange. But the same line of reasoning would have us call an airplane a medium of transportation. Likewise with a bus, train, bicycle, roller skates … even a pair of legs night be called a medium of transportation, but our definition is apparently vague. So money

must be more concretely defined … unless of course there is no such tangible thing as money.

Aha! Suddenly we realize SOMETHING must be used AS money, and that money

in and of itself does NOT exist. The Coinage Act of 1792 and the United States Statute Codes BOTH declare thus:

The money of account of the United States shall be expressed in dollars …

31 U.S.C. 371 and Coinage Act of April 2, 1792, Section 20.

Dollars

are NOT the money … but the expression of the money. Similarly, concrete is expressed in cubic yards, but there are no foundations built out of cubic yards of cubic yards. Concrete (the entity) is EXPRESSED in cu. yds. (unit of measure) and nobody would expect to pay a concrete company for cubic yards WITHOUT getting the concrete.

So what is the MONEY of account of the United States?

No State shall … make any Thing but gold and silver Coin a Tender in Payment of Debts …

Article 1, Section 10 United States Constitution.

… the proportional value of gold to silver in all coins which shall by law be current as money within the United States.

Coinage Act (1792), Section 11.

The terms ‘lawful money’ and ‘lawful money of the United States’ shall be construed to mean gold or silver coin of the United States:

12 U.S.C. 152

What then is a dollar

? It is a UNIT OF MEASURE, with all of the substance of an inch

or a foot

or a pound.

Dollars

do not exist as a tangible thing. There are no inches of inches, feet of feet, pounds of pounds or dollars of dollars. A dollar

is not a piece of paper, nor is it a coin. It is not a THING, only a unit of measure.

Likewise money

is an abstract, an idea, not an entity. Something can be used AS money (e.g. silver, gold, corn, etc.) but there is no such thing (in and of itself) that is money.

Federal law declares gold and silver to be used AS money and to be EXPRESSED in dollars,

with a dollar

of gold being [1/42 troy oz.] fine gold (31 USC 449, 314, 821) and a dollar

quantity of silver 371.25 grains pure (Coinage Act 1792).

Since the term dollar

was a unit of measure expressing still another unit of measure (troy oz. and grain), most Americans came to regard the dollar

as the THING for which it was only the unit of measure. Mysterious forces crept in unawares

managed to remove the thing

and substitute the unit of measure (no-thing

) thereby destroying our economic foundation. We are pouring foundations measured in cubic yards

… but somebody stole the concrete!

Over the years we have been blessed

with a variety of dollars

; one of gold (the smallest coin minted in the U.S.), one of 90% silver, one of 40% silver (some Eisenhower $

s), one of standard dimension with NO silver (Eisenhower), the NO NOTHING super quarter

called the Susan B. Agony

and the real cheapskate PAPER dollar.

As the dollar

was fashioned from cheaper materials, the prices

mysteriously began to rise … some calling the phenomena … inflation.

A more realistic way of looking at this might be to say that the money of account

(gold and silver) was progressively removed from circulation, being substituted by cheaper substances, yet retaining the asserted value by fiat or declaration. Since the public still THOUGHT the money

was the same, the money of account

became an IMAGINARY nonentity as a result of progressively greater seigniorage (difference between face value and free market value). Our money of account

is now 100% seigniorage as we will see more closely later in this text. At any rate, the 90% silver coins have been debased to tokens of copper/nickel with no silver. Shouldn’t products cost more in copper/nickel dollars

than in silver dollars

?

Lenin is said to have declared that the best way to destroy the capitalist system was to debauch the currency.

John Maynard Keynes — Economist

Throughout history, man has used many different things as money (e.g. cows, salt, cowry shells, tea, opium, tobacco, rice, stone wheels, iron, gold, etc.) but despite their dissimilarity, they all possessed a unifying characteristic; they were all wealth. And wealth is TANGIBLE.

Now if dollars

measure silver and gold, and States are required to settle debts in these precious metals … WHERE IS the silver and gold? It was stolen by some very clever folks in a most subtle manner, but we'll cover that later. First we must understand some very basic economics.

Trade (commerce) has been the motivating force behind the establishment of money,

and as the volume of trade increased, there was a change in the substance that was used as money, especially as man developed the talents of processing ores and fashioning coins. Let's consider a simple illustration to demonstrate the need for an exchange medium. Joe would like to buy 2 goats from Bill and is willing to pay

1 sheep. But Bill doesn’t want any sheep but would like to have a cow. Dilemma! Joe has no cows … but! Harry has oodles of ‘em. New Deal (not to be confused with FDR)! Joe is able to trade 2 sheep for 1 cow. New dilemma! If 1 cow = 2 sheep and 1 sheep 2 goats, 1 cow must = 4 goats. Therefore: 2 goats (what Joe wanted in the first place) must be ½ cow. But without a freezer Bill will have little use of ½ cow. Idea! Joe offers Bill an intermediate substance called salt, and Bill accepts since he recognizes the swap-ability

of salt. Bill could then offer this salt (plus a little more) to Harry in exchange for a cow. Salt was used as money since it was the medium of exchange.

Salt money gave way (thank heavens!) to silver and gold which have been acceptable worldwide as money for over 3,000 years.

Gold and silver (wealth) were slowly replaced by money

(imaginary demand) in such a way the public was either unaware or even an accessory to the fraud. In ancient times, a goldsmith (forerunner of the modern banker) would store peoples' gold for safekeeping (and a fee). He soon discovered that few people reclaimed their gold (relative to his stock) since it represented surplus (savings), and being shrewd (euphemism for crooked) the goldsmith began to lend

out a considerable portion of the gold for a fee or interest,

keeping just enough (sometimes) to cover his hind end (depositors). Banking (lending) soon replaced saving (banking). Something else was discovered. The receipts (issued by the goldsmith to the depositors) soon began to circulate as currency

since they provided convenience

but could still claim the gold through redemption, provided the crook in the middle still had some in his vault. Similarly, in the U.S., proxy certificates began to circulate in lieu of the gold and silver coin, but they could always (so we thought) claim the precious metal they represented … that is until somebody decided to close the gold window

in 1933 and the silver window

in 1968.

At one time, bankers were merely middlemen. They made a profit by accepting gold and coins brought to them for safekeeping and lending them to borrowers. But they soon found that the receipts they issued to depositors were being used as a means of payment. These receipts were acceptable as money since whoever held them could go to the banker and exchange them for metallic money.

Then bankers discovered that they could make loans merely by giving borrowers their PROMISES TO PAY (bank notes). In this way, banks began to CREATE money. More notes, could be issued than the gold and coin on hand because only a portion of the notes outstanding would be presented for payment at any one time.

Demand deposits are the modern counterpart of bank notes. It was a small step from printing notes to making BOOK ENTRIES to the credit of borrowers which the borrowers, in turn, could ‘spend’ by writing checks.

Modern Money Mechanics, pub. by Federal Reserve Bank of Chicago, p 3,4 (emph. mine)

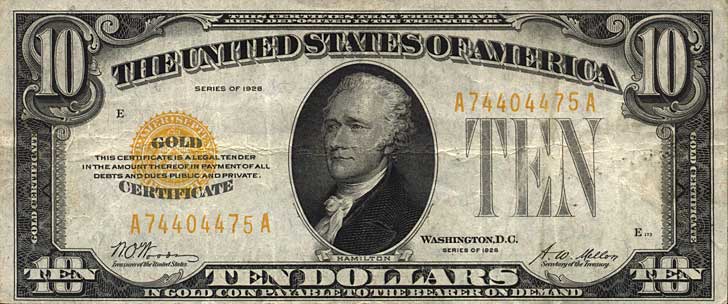

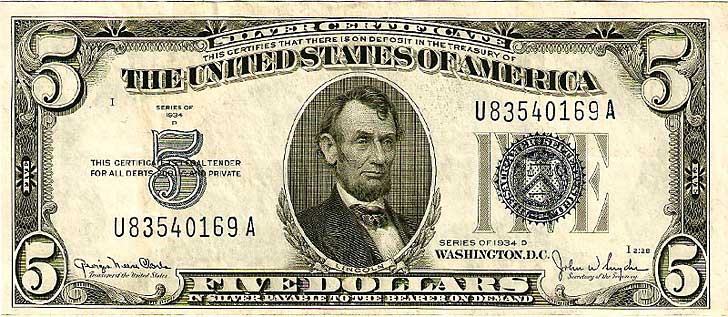

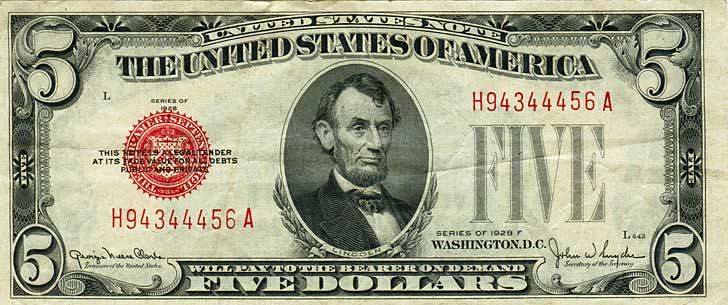

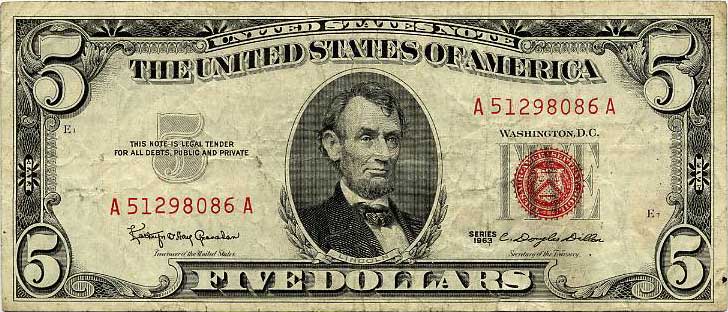

And until 1963, all paper currency in circulation NEVER claimed to be the money,

nor did it claim to be DOLLARS. The paper was REDEEMABLE in SILVER or GOLD EXPRESSED IN DOLLARS. The following examples will illustrate this point.

Below, are four specimens of paper currency, the top three of which are lawful negotiable instruments (or notes) in that they identify WHO is paying, WHAT is being paid, to WHOM, and WHEN (see Black’s Law Dictionary). The bottom note does NOT conform to the lawful definition of a note!

Looking for a moment at the bottom two notes, we will reason this out. If the upper (of the two) note claimed The United States of America … will pay to the bearer on demand … FIVE TOMATOES,

it would still be a lawful note (even a lawful contract). If, however, the words will pay to the bearer on demand

are removed (as in the bottom specimen), would that convert the piece of paper into FIVE TOMATOES?!

Paper currency issued & printed by U.S. Government

Paper Currency Issued by the Federal Reserve Banks (Private Corporations) but still printed by the U.S. Government

currency,the gold or

lawful moneyis the

money.After gold was

outlawedin 1933/34, FED notes would only redeem

lawful money(12 USC 152 says lawful money is …

gold or silver coin.)

dollars,PRETTY CLEVER, Huh?

Through guarantees that ‘paper money' could be exchanged for something of intrinsic value, gold served to inspire a measure of CONFIDENCE in the system.

Gold, pub, by Fed. Res. Bank of Philadelphia, p10 (emph. mine)

What gives? These six different (they are different aren’t they?) specimens ALL claim to BE dollars. But a dollar

is a UNIT of our money of account. Could we possibly have six different kinds of inches? Or gallons? Or ounces? Or minutes?

|

90% pure gold (one dollarquantity). |

|

90% pure silver (one dollarquantity). |

|

40% pure silver (can it be a dollarquantity?) |

|

No silver, only copper/nickel |

|

No silver and only 50% more copper/ nickel than a QUARTER, yet it has 400% of the purchasing powerof a quarter! |

|

Paper & Ink dollarthat cannot BE a dollar,and does not represent a dollarquantity of anything! |

13Thou shalt not have in thy bag different weights, a great and a small. 14Thou shalt not have in thine house different measures, a great and a small. 15But thou shalt have a perfect and just weight, a perfect and just measure shalt thou have, That thy days may be lengthened in the land which the Lord thy God giveth thee.

Deuteronomy 25

Having removed the phrase will pay to the bearer on demand

on their most recent Federal Reserve Notes (after 1963) has saddled the American people with a dilemma. Debts have become perpetual as there is nothing with which to settle them. Notes are evidence of debt, and changing the wording to make the note APPEAR to be the settlement does not alter that fact. Let's see if we can clarify this situation.

Most of us are familiar with the adage A man is no better than his word.

But Christ said By their fruits ye shall know them.

Since the deed frequently conflicts with the word, we must recognize Christ's statement as the more accurate. For example, an I.O.U. is a man's admission of debt, but his I.O.U.s are worthless if he refuses to make them good by fulfilling his obligation. A bank or treasury note (paper money

) is also an admission of debt, but unless the issuer (Federal Reserve Banks and U.S. Treasury AND commercial banks that create deposits) redeems his I.O.U.s (notes), they too are frauds and represent' COUNTERFEIT. Likewise, a check is received as a promise of payment, but if there is nothing in the account on which the check is drawn, they represent bogus claims.

Prior to 1968, when silver redemption was repudiated by the issuers of these notes, we could demand payment of the silver for which the notes were issued. By that time there were far too many notes against the silver, but the rubber check

writers knew our faith was firmly established in the paper promises.

Now we labor to produce wealth, give up our wealth to get the paper, and the money creators

refuse to give up anything if we give the paper back.

Before 1933, the holder of a $20 gold certificate could swap it even for a $20 gold piece (approximately 1 troy oz fine gold). Now the banking system will swap a $20 gold certificate for a $20 FED NOTE, but will not issue any gold in redemption. But if we would like to buy

some gold from another citizen (a non-banker), we would currently need at least twenty-five more $20 FED NOTES to obtain just 1 gold coin carrying a face value of $20. Redemption is made possible when the CREATOR (issuer) regains possession by REPURCHASE. Christians recognize the fact that THEY do not redeem one another, but that the CREATOR must be the redeemer. Likewise, a check writer redeems his OWN checks. We don’t try to palm the checks off onto another sucker like we do with Federal Reserve Notes.

By refusing to redeem their notes, the Federal Reserve and Treasury both acknowledge bankruptcy. They know it. The European finance ministers know it. The Arabs know it. The only people who do not yet comprehend are the American victims whose silver and gold was stolen by the few people granted the power to print paper money

at no cost to themselves and then use these instruments

to steal our wealth. Yet the American people still REFUSE to believe they were robbed, and that the robbery continues!

Lenin was certainly right. There is no subtler, no surer means of overturning the existing basis of society … The process engages all the hidden forces of economic law on the Ode of destruction, and does it in a manner which not one man in a million can diagnose …

John Maynard Keynes

Fortunately, that one man in a million emerged, known by Monetary Realists as Merrill M. E. Jenkins, Sr., who cleared the air of economic smog and double talk, devoting the last 14 years of his life to the exposure of MONEY

… the Greatest Hoax on Earth.

But since the nature of coin, credit and circulation is still unknown to the vast majority of people, we continue to grind on towards oblivion, amassing fantastic debts amidst prosperity.

Long before we wake up from our dreams of prosperity through an inflated currency, our gold which could have kept us from catastrophe will have vanished, and no rate of interest will tempt it to return.

former Senator Elihu Root

Our federal, state, municipal, corporate and individual debts now total some $13 Trillion and CANNOT be paid off

EVEN IF WE NEVER BORROWED ANOTHER CENT. Debts (monetized) cannot pay off debts. All money

is created by the banking system, is then LOANED into circulation at INTEREST … and we CANNOT return to a sole source MORE than we received from it. They only loan the principal. There is not the total money

in circulation to pay off all the cumulative principal and interests. We must borrow

more and more of this imaginary money

to service existing debts, thereby creating new principal on which to pay interest, yet those people manning the shovels

fail to understand why the hole keeps getting deeper.

Our rampant materialism has spawned a new slavery in America. The average individual is so far in debt he fears the loss of his paycheck, without which he would be unable to continue the payments on his home, automobile, camper trailer, boat, airplane, motorcycle, snowmobile, etc, etc. Having been tempted by easy payments, nothing down, buy now, pay later

slogans, the average American has succumbed to the bankers’ fiscal heroine.

In 1945 non-farm families owed $5.7 billion, consisting primarily of installment debt. By 1974 the debts had risen to $190.1 billion — a leap of 3,235 percent.

William E. Simon (A Time for Truth)

Ever increasing taxes take a further toll on us as we service

the debts being amassed by our governments, while debt service makes up a large portion of consumer prices,

in some industries as much as 77%. We have already lost our independence, the banks already own our country and we have lost OURSELVES, mortgaging our very souls to the creators of paper tokens we erroneously call dollars.

For what shall it profit a man if he shall gain the whole world, and lose his own soul?

Mk. 8:36

Debt is SLAVERY! Make no mistake about it. Many a debt ridden man tries to hide his misery by feigning success or tries to escape with alcohol or drugs … even suicide. King Solomon, a man who had everything (he had 700 wives and 300 concubines, he must have had everything else!) and was noted for his wisdom, wrote in Proverbs 22:7

The rich ruleth the poor, and the borrower is the slave to the lender.

Wow! The Bible even serves us as a financial newsletter!

To obtain a clearer understanding of debt/interest as it applies to our monetary system,

we must intrude upon the sacred ground of the Federal Reserve System and shed some light on this enigmatic obfuscation.

And ye shall know the truth, and the truth shall set you free.

John 8:32

The FED, as this institution is called in financial circles, was chartered by an Act of Congress (December 23, 1913), the same year we were saddled

with the 16th Amendment (income tax). Few are aware that the FED is a PRIVATE CORPORATION, granted tax exemptions (government need not be exempted as it pays no taxes anyway), pays

postage (the government uses a Federal frank) and has their telephone listings under F,

NOT under U.S. GOVERNMENT. The twelve FED Banks are governed

by the Board of Governors, which office DOES use a Federal frank for postage. The Federal Government does not own any stock in the FED System and has NEVER been able to audit the FED despite numerous attempts.

The FED is operated for profit … man is it ever! And that the FED is illegal seems to matter little to our esteemed representatives who swear to uphold the document that declares the FED unlawful.

Congress shall have power … To coin Money, regulate the Value thereof.

Article 1, Section 8 United States Constitution

CONGRESS!, not a PRIVATE CORPORATION, shall have the power to COIN money, not PRINT paper tokens representing NOTHING! And Article 1, Section 10 of the Constitution declares the MONEY shall be GOLD AND SILVER COIN.

Congress, in delegating a power IT did not have, has given the money

creators the POWER TO TAX! It costs absolutely NOTHING to print paper money

! All overhead is paid for

with pieces of paper rolling off those machines. We must give up someTHING to get these certificates of confiscation,

thereby paying a TAX to a private corporation. Figure it out. Paper money

is the tool used to expropriate the wealth from the people who PRODUCE the wealth, BY the people who CREATE the paper for NOTHING!

Most economists resist the suggestion of 100% redeemable currency and no fractional reserves, since such a suggestion severely restrains credit (debt) expansion. Simply stated, banks would be unable to lend what they DO NOT HAVE, which unfortunately (for US!) is exactly what banks are doing!

Thus our national circulating medium is now at the mercy of loan transactions of banks … which lend, not money, but promises to supply money they do not possess.

Prof. Irving Fisher (100% Money — 1935)

Back in Mr. Fisher's day, there was still some money of account

in circulation (and in reserve); however, since 1968 there has been no lawful money

available to the citizens whose property it once was. While it is true that gold and silver coin does exist, it has been made available by the non-bank public, some of it reportedly sold to the Treasury which resold it at auction to keep up the image of reserves.

Money

does not exist as a tangible THING, but is only an IDEA applied to a THING (such as silver, or gold, cows or salt).

The actual process of money creation takes place in commercial banks.

Modern Money Mechanics published by Federal Reserve Bank of Chicago. page 3

The FED is technically correct in this statement, since the word create

means: to bring into being; to cause to exist. (see Webster) Man cannot create anything. We can only transform things (e.g. a tree becomes lumber … but as Joyce Kilmer said in the poem Trees, only God can make [create] a tree.

). However, we can create ILLUSIONS, such being intangibles having the substance of mermaids.

Neither paper currency nor deposits have value as commodities. Intrinsically, a dollar bill is just a piece of paper. Deposits are merely book entries.

Modern Money Mechanics, page 3

Get that? Deposits (checking accounts, savings accounts, etc.) are MERELY BOOK ENTRIES! How tangible is a book entry? How much do they weigh? These numbers (entries) do not measure anyTHING. There is no wealth deposited in a bank. There are no dollars

of anything there!

What then, makes these instruments — checks, paper money, and coins — acceptable at face value …? Mainly, it is the confidence people have that they will be able to exchange such money for real goods and services whenever they choose to do so.

Modern Money Mechanics page 3

WOW! A CONfidence game of the highest magnitude. I'll bet you thought there was someTHING somewhere to impart value

to the tokens (paper and metal) we carry around with us.

Confidence in these forms of money also seems to be tied in some way to the fact that assets exist on the books of the government and the banks equal to the amount of money outstanding, even though most of these assets themselves are NO MORE THAN PIECES OF PAPER (emph. mine) … and it is well understood that money is not redeemable in them.

Modern Money Mechanics page 3

Are you beginning to comprehend this madness yet?

Banks lend by creating credit. They create the means of payment out of nothing.

Ralph M. Hawtrey (former Secretary of British Treasury)

Here is how banks (commercial) create

that non-substance called money.

Operating on a fractional reserve

(currently about 15% on demand deposits or checking accounts), the banks multiply deposits,

receiving our currency (e.g. $1,000) and loaning

us $6000 they do not have (in the form of a deposit CREDIT). The $1,000 in the vault covers the depositor, the $6000 they loaned

was invented. Banks do not loan anyTHING! They rent ILLUSIONS! Neat huh? You know a fella could get rich doing that! And to think the borrower

has to pay back

the loan he never got … PLUS INTEREST! And then comes the frosting on the cake. The bank wants a lean against wealth owned by the borrower.

Now isn’t that a sweet swindle! The borrower pledges WEALTH to get dollars,

but the banks will not issue WEALTH to redeem those dollars.

Some call that a one way street.

Reserves on time deposits (savings, etc) range from 3% to 7% (non-personal time deposits of 4 years or more require 0%), but using 5% for easy figuring we can deposit $1,000, the bank can create 19,000 new, dollars

which we may then borrow

if we meet the bank's impeccable standards. Man! What a deal! But wait!

What are the reserves? Why, the reserves are PAPER … what would we expect in a modern, highly sophisticated, technological society such as ours? Gold is old fashioned.

It requires effort to obtain while paper can be printed at astronomical rates … and it is SO EASY.

And these FED Notes we all carry around are printed by the Treasury (at no cost) and created out of the razzle-dazzle of bond issues (more paper), FED Notes (more paper I.O.U.s) and a dose of mystery.

First, the Treasury creates a bond (fancy word for I.O.U) and sells

it to the FED which in turn creates a checking account for the Treasury and credits the account whatever the amount of the bond. The Treasury then prints the $ notes, gives them to the FED (to cover the checking account) and begins to spend

these I.O.U.s to buy up our production. The Treasury must then pay back the principal, plus interest, and derives the money from the taxpayers, or they may sell

MORE bonds to the public in higher denominations and use these to redeem existing bonds reaching maturity. The FED gets the principal plus the interest at a cost of nothing. In other words, the government gives I.O.U.s to the FED which opens up a phony checking account for the government to write phony checks against the phony account the FED created when it bought the I.O.U.s with the phony money the FED asked the government to print! Very creative fellas!

Government is the only agency which can take a useful commodity like paper, slap some ink on it and make it totally worthless.

Ludwig von Mises —economist

What about the gold in Fort Knox? Don’t the notes get their value from that gold stockpile? Well, not exactly. The Treasury doesn’t own any gold, having sold

it to the FED which bought

it with the paper. When the FED was established, the gold reserve requirements were set at 40%, allowing the system

to issue a receipt (certificate) for the gold being deposited by the public, and 1 ½ newly created

phony claim checks against the same gold for which there was already a claim check outstanding. These new phony receipts were loaned out at interest and could later be swapped for the certificates, which were a direct claim on the gold. After all, one dollar

($) looked like any other dollar

($) once it was entered on the ledgers of the banking system (of plunder). For instance, a one dollar

gold coin placed in a savings account would produce an entry of — $1.00. It and a one dollar

silver coin deposited in the account would produce an entry of — $1.00, and a one dollar

piece of paper (which THEY created for NOTHING) when deposited in the same account would produce an entry (on their books and the savings account book) of — $1.00. Funny, on paper they all looked the same … and in just 20 years, the FED had created enough of their own phony claim checks against depositors’ gold that they were able to convince

our President

to outlaw public ownership of THEIR OWN GOLD! And it was called in

(1933) to stabilize the dollar.

But the dollar

was (is) a unit of measure. Could FDR have stabilized the mile

? Or the ounce

? Why did the American people allow the government to seize their gold (and then transfer custody of it to the private FED Banks)?

Could it have been the scientifically created depressions

referred to by Congressman Charles A. Lindbergh (Sr.) as a result of the Federal Reserve Act? Could it be possible that the FED CREATED the Great Depression

of ‘29 to condition the public for subsequent events?

The reserve requirement (specie reserves) was later lowered to 25%, and this accelerated the close-out

of silver by creating a certificate (receipt) for silver deposited … and 3 new phony claim checks issued against the same silver. In 1963 the FED began issuing the first of its NO PROMISE notes (the day after JFK was assassinated) since there was not nearly enough silver to redeem the circulating paper dollars.

In 1965, the Treasury began coining NO SILVER tokens to replace our lawful money,

and by mid-1968, the FED and Treasury repudiated REDEMPTION of silver certificates. The gold was stolen in ‘33 and the silver was stolen in ‘68. What is now the money of account

of the United States currently expressed in dollars

?

Fractional reserves have netted us another bonus

that is frequently overlooked. All the new phony dollars

the banks created (and are still creating) has increased the number of purchasing units

resulting in higher prices.

Oh swell! We put our loot in the bank and they inflate it to create loans. We've been digging our own graves!

Doesn’t the output of the nation (expressed as gross national product) back

these notes? No way. Gross National Product (GNP) is nothing more than the sum of dollar

transactions. For instance, if Joe gets a haircut for $5 and the barber spends the $5 for supplies, the GNP is $10. If the supplier uses the $5 to buy some ball point pens, the GNP becomes $15. The annual GNP exceeds $1 Trillion, but about one-third of the GNP is interest on collective debt! We cannot expect to impart value to I.O.U.s by listing more I.O.U.s as backing.

Further, a large portion of the GNP is LABOR, but after the labor has been performed … it's gone! But the I.O.U.s are still floating

around in the economy. So that backing is gone too! Another portion of the GNP represents PRODUCTION … but once a product has been produced, it either depreciates, rots, decays or is consumed, yet the notes continue to pile up … unless the FED decides to restrict loans

and contract the supply of credit

… whatever that is. The only thing that gives this paper money

value is the CONFIDENCE people have in it.

Paper money is MADNESS. It costs ABSOLUTELYNOTHING to print it! All overhead of the money creators

is paid

with little pieces of paper. It is OUR labor and OUR production that gives these pieces of paper their ability to CONFISCATE wealth. The only real effort expended by the issuers of these bogus checks is in keeping us from finding out we are being robbed! They heap us with platitudes arising from out of the depths of the science of PLUNDER … known as economics.

One reason why economists are in such disrepute is that they have pretended to understand inflation and how to control it, when obviously we do not.

Wassily Leontieff, Nobel Prize winning economist — N.Y. Times 1/30/77

The rules of economics don’t seem to work like they are supposed to.

Arthur Burns, Chairman of the Federal Reserve Board — N.Y. Times 1/30/77

In the booklet Story of Money (Federal Reserve of N.Y.), there are three different forms of U.S. money

identified as being in use, those being: COIN, worth about $11 billion.

PAPER CURRENCY, worth about $105 billion and consisting almost entirely of Federal Reserve Notes,

and CHECKBOOK MONEY, about $270 billion in 1979,

giving us a 1979 total of $386 billion of token money. With banking assets

in America totaling some $1 TRILLION, one might ponder for a moment where the dollars

are that represent the approximately $614 billion balance that are listed in bank ledgers. But then we might also ponder the question of cashing

the CHECKBOOK MONEY ($270 billion) with the remaining COIN and PAPER CURRENCY (a combined total of $116 billion) which leaves us a little short! 154 billion dollars

short! But when we study the function of a check, we must realize that it serves as an ORDER to a bank to pay someone some dollars.

Since there are far more checkbook dollars

than FED notes to cash them, we must conclude that many checks are never really cashed.

If, for example, a housewife writes a check to a supermarket for groceries purchased, the supermarket will generally deposit that check with their bank, which in turn will credit the supermarket's account. The supermarket will issue checks to their suppliers against the credit, and the suppliers likewise. The bank's merely enter credits and debits of NUMBERS of nothing. They certainly don’t transfer LAWFUL dollars

of gold or silver!

The cashing

of a check leaves us with FED NOTES … which are declared to be LIABILITIES

of the FED banks, and all notes are now NON-redeemable for coin containing silver, or gold, or anyTHING.

Wow! Who wouldn’t like to write I.O.U.s and have them declared MONEY! The FED lists their notes as liabilities in their financial statements (asset liabilities) and then declares in their publications that demand liabilities of commercial banks are money too! But most people think money is an ASSET! But the removal of specie redemption transformed money

into LIABILITIES … and we must borrow these liabilities into circulation!

As noted earlier, demand liabilities of commercial banks are money.

Modern Money Mechanics page 3

And what of the $11 billion in COIN said to be in circulation? Are they really worth

$11 billion as the FED says?

Coins do have some intrinsic value as metal, but far less than their face amount.

Modern Money Mechanics, Federal Reserve of Chicago page 3

Can a Susan B. Agony

coin claiming to be 100 cents be worth

that amount when the Fed/Treasury says they cost but 3 cents to produce. Who gets the other 97 cents? And if the FED/Treasury team — can create all the notes they want for free, then do the coins end up costing them anything at all? With what do they purchase the metals? DOLLARS?

This is a staggering thought. We are completely dependent on the commercial banks. Someone has to borrow every dollar we have in circulation, cash or credit. If the banks create ample synthetic money we are prosperous; if not, we starve.

Robert H. Hemphill (Credit Mgr., Federal Reserve Bank of Atlanta)

Since all dollars

are borrowed into circulation, we should consider the meaning of the word BORROW.

borrow: to receive with the implied or expressed intention of returning the same or giving an equivalent.

Webster

What do we borrow from a bank? The money of account (by law) is silver and gold. Do we borrow silver and gold? Nope! We do not receive anyTHING from a bank, other than a piece of paper with numbers representing a CREDIT.

What does credit look like? How can a borrower borrow

anything unless he receives it?

Could a lawn and garden center loan out a roto-tiller without giving up the tiller? Can a piece of ground be tilled with a rental agreement? Could a rental car company loan (rent) an automobile without the renter receiving the car? Ever try to drive a rental agreement? In all instances, when we rent or borrow something, we EXPECT to GET THE THING! But somehow, banks are regarded as different.

They have managed to con us into believing a piece of paper with numbers printed on it is the THING we borrow! Any dummy with a TYPEWRITER can print numbers just as nice (and meaningless) as theirs! Banks don’t loan MONEY (of account). They loan CREDIT! But whose credit do they loan? What does it look like? How much of it is a dollar

quantity?

A national bank has no power to lend its credit.

Farmers & Miners Bank vs. Bluefield National Bank, W. Va., 11F 2d 83, 271 USC 669

Since ALL dollars

are created by the commercial banks and the FED system, and since we must return those imaginary dollars PLUS interest (more phony dollars), we must conclude that collective payoff is IMPOSSIBLE. We cannot return to a single source MORE than it created. The total debt exceeds the number of created dollars,

since the banks only loan the principal but do not give us the additional dollars

to pay off the interest on something we never got. And with a combined public/private debt in the U.S. of some $13 TRILLION, we find ourselves paying some $650 BILLION in ANNUAL INTEREST (@ only 5%!), or about ONE-THIRD of our GNP (annual production). We are broke! The nation is BANKRUPT because these I.O.U.s cannot pay off a debt, the debt is merely transferred and cannot be cleared.

The promissory note, even when payable on demand and fully secured, is still, as its name implies, only a promise to pay, and does not represent the paying out or reduction of assets.

Don E. Williams Co. v. Commissioner of Internal Revenue, 51 L Ed 2d 48 and case #75-1312

Time to regroup! Where are we?

Money

is an abstract term applied to a TANGIBLE thing, making that thing (e.g. salt, tobacco, gold, etc.) themedium of exchange.

- The

money (medium of exchange) of account

is silver and gold. - But it was stolen by the

papermakers.

Dollars

are units of measure and express themoney.

- The banking system

creates

money. (An abstract idea … a non-tangible) - We work to get this money that was

created

for nothing. - Then the banks charge us interest on this

creation.

- There is not enough

money

in circulation to pay off all of the outstanding debts. Moremoney

must be borrowed into circulation to pay off the previous loans, thereby increasing the debt PRINCIPAL on which MORE interest must be paid. - The more we

borrow,

the more wereceive.

The deeper in debt … the richer we get! - Our

money

is DEBT (credit/liabilities). We have MONETIZED DEBT!

Banks create money by ‘monetizing’ the private debts of businesses, individuals and governments. That is, they create amounts of money against the value of those I.O.U.s.

I Bet You Thought, Federal Reserve Bank of N.Y.

In addition to securities, the federal government issues non-interest-bearing DEBT — currency or PAPER MONEY. Currency is so widely accepted as a medium of exchange that most people do not think of it as DEBT.

Two Faces of Debt, pub. by Fed. Res. Bank of Chicago, p 4 (emph. mine)

Imagine! Debt is money! And the FED NOTES are debts, as are customers' accounts of commercial banks. And when we borrow money (debt) from a bank, we are liable for the repayment (of the debts) so they become OUR liabilities too! What kind of bookkeeping system is this country using anyway!? Both assets and liabilities are liabilities! But the FED says debts are assets.

(s of Debt, Federal Reserve) Wowee! FED notes are by definition (of a note) liabilities of the FED, but despite the fact they owe us something for them, they will not pay us anything for them. But then we must BORROW these liabilities (I.O.U.s) from the bank, hence they become OUR liabilities at the same time. They are I.O.U./U.O.Mes. Will miracles never cease! These are indeed extremely clever devils!

Examining a FED note, we read the words: Federal Reserve Note as they appear across the top. The word FEDERAL implies Federal Government. Is it? No, it is a PRIVATE bank. The word RESERVE implies an excess (presumably wealth) of something to give the money

value. What are the reserves? Mostly paper I.O.U.s. The word NOTE implies an enforceable contract. But is it? A note (by law) must identify WHO is paying, WHAT is being paid, to WHOM and WHEN. Since the issue of new series notes starting in ‘63, they have not stated the WHAT, WHEN and to WHOM. The NAME alone is a three way FRAUD. Talk about truth in lending!

To the left of the picture and above the FED bank seal, we read:

This note is legal tender for all debts public and private.

A note IS a debt! How can a debt pay off a debt? And what is legal tender

? It is LEGAL to TENDER (offer) these phony claims (against nothing) and we will not go to jail for passing counterfeit. These are legal deceit receipts!

Now for the piece de resistance. Along the bottom of the note, emblazoned for all starry eyed worshipers of mammon to see, are the words: X no. of dollars.

Oh what a classic! On top they declare it is a NOTE. On the bottom they declare it to be a quantity of the thing (they say dollars are the money) for which it is a note! They admit a debt and settle it with the same piece of paper! What a time-saver!

But wait! What makes a $100 bill worth any more than a $1 bill? They are both the same size, weigh the same, require the same amount of effort to produce, etc. They both cost them nothing, represent nothing and are redeemable for nothing. How can one piece of paper be worth 100 times as much as the other? If for example, a tuna is a fish, wouldn’t 100 tuna have to be 100 fish? And if a dollar

is a piece of paper (they said it!), wouldn’t 100 dollars

have to be 100 pieces of paper? Can we think of just one entity that can exist in multiples WITHOUT increasing in number?

Perhaps this all seems like an exercise in semantics. Most people believe the system works,

although they aren’t sure how well. Our grandparents lost their gold, our parents lost their silver, spawning a new generation adrift on a sea of perpetual and ever increasing debt that CANNOT (and eventually WILL NOT) be paid off. Foreclosure is rampant throughout the land of milk and honey.

Our standard of living is in decline as debt soaks up our productive capacity at a staggering rate. Government (at all levels) tempts us with their bond issues (more I.O.U.s), thereby drawing off our own notes of confiscation

so we can’t bid them in the marketplace for our own production. This is the REAL purpose of bond sales … for after all, the Treasury PRINTS these notes and certainly doesn’t need our old worn out ones. Businesses borrow and refinance (roll debts) in the scramble to keep pace with competition (which is expanding on credit) and government regulation (e.g. pollution control projects) extracting the payments from the public by raising prices, while the individual borrows more and more in attempt to have the things his parents owned free and clear.

All people are chained down to heavy toil by poverty more firmly than ever they were chained by slavery and serfdom; from these one way and another, they might free themselves, these could be settled with, but from WANT they will never get away.

from 3rd Protocol, Learned Elders of Zion

Without the naturally restraining element of 100% wealth redeemable media, governments (despotic tyrants) can print money at no cost to themselves and can purchase

our production (wealth) and can outbid us in the marketplace, eventually reducing us to poverty and dependence upon them for all our basic necessities. As we watch the food-stamp program, welfare payments, old age housing projects, etc., it may be recognized by some people, that a large (and growing) portion of our people are ALREADY DEPENDENT upon the papermakers for their daily bread. But those of us still in the workforce are the PRODUCERS of goods; the powers that be

simply use the money

as the medium of confiscation

and are thus able to extract our wealth and distribute it AS THEY SEE FIT, without our consent, and AGAINST our wishes as expressed in letters to our elected

officials. Our government is not financed by the taxpayer

despite all the claims made by conservatives

concerning wasted taxpayers' dollars.

Taxes are used to REGULATE the economy in a system of FIAT money. Taxes are NOT used to FINANCE our government!!!

If however, a government refrains from regulation and allows matters to take their course … the worthlessness of the money becomes apparent, and the fraud upon the public can be concealed no longer.

John Maynard Keynes (Economic Consequences of the Peace, 1920)

Please UNDERSTAND! Governments that PRINT paper money

do not need our paper money,

They can print whatever they want … and all overhead is paid

with a single piece of paper (called a government check). They need our WEALTH and obtain it by offering us their pretty PAPER which they CON us into thinking was obtained by them the same way we got it … effort. Otherwise we wouldn’t be so foolish as to give up our wealth (production by labor) in exchange for paper that cost them NOTHING. Taxes serve two distinct functions in a FIAT economy. They reduce the amount of money

we can bid for what WE produced, thereby allowing our government to easily outbid us without having to flood the market with unnecessary amounts of paper,

and they reinforce our belief that we finance our government and that the government needs our paper … which it can print for nothing. You see friends, if the worthlessness of the money becomes apparent,

we will refuse to take it, and we will no longer give up our WEALTH to get it, and government will then become OUR SERVANT instead of OUR MASTER. And until we return to a wealth medium of exchange (e.g. silver, gold) the government will hold us in contempt

and will do as it pleases … taxpayer be damned! These FED notes are I.O.U.s! Why should the government want the FED bank's I.O.U.s? And why should the FED want them? Would you cherish your own I.O.U.s?

Our money

IS inflation, not the INCREASE of it … but ALL OF IT! The increase of the money supply

makes the inflation VISIBLE, but all our money

is just IMAGINARY DEMAND chasing after REAL GOODS AND SERVICES, and represents 100% CONFISCATION in favor of the issuer of the I.O.U.s.

Were it not for taxes and interest drawing off some of these phony dollars,

we would be buried in the stuff, and the fraud upon the public could be concealed no longer.

Prices would go through the roof overnight. If just ½ of 1% of the total banking assets

(over 31 trillion) were withdrawn and bid in the marketplace, PRICES WOULD DOUBLE IN JUST 24 HOURS! The FED is doing everything possible to keep us from spending our own purchasing units. They tie up our funds in Certificates of Deposit, offering us high interest

as an inducement, but the interest does not match the cost of living

increase. They tempt us to lock away

funds in NOW

accounts (using low interest as an inducement) and resell

us BONDS (euphemism for I.O.U.s) in exchange for our I.O.U.s, and keep our notes out of the market where they might do US a little good … stealing from each other.

The system is set on destruction of humanity, and we are the eager ones sowing the seeds of our own destruction goaded by greed now … and survival later. We're too shallow minded to remove the chains of slavery; we would rather drape them on our neighbor and let him worry about it.

So far has this FRAUD (Federal Reserve Accounting Unit Devices) been carried, we may soon see a deflation and re-issue

of new money

just to make the numbers MANAGEABLE. Germany did this in 1923, requiring the people turn in 1 TRILLION old Marks

to get 1 new Mark

; the old paper became so useless the housewives burned it in their wood stoves because it was CHEAPER than wood! (see The Story of Money, FED Bank of N.Y., page 20)

The banking system is the SOURCE of this worthless paper, loaning every stinking dollar

at interest … which cannot be paid unless another loan is made available to create enough dollars

to cover the additional burden of interest. Debts continue to rise until DEBT SERVICE consumes all of our production, taking everyone (non banker) to the cleaners on the day of judgment.

This may seen incongruous to some folks. After all, there are people who have no personal debts, while others are within reach of solvency. Surely, they reason, some of us will escape this calamity. But notice, even though we may be without a personal mortgage, our

government has taken one out on our property for us! Our property is pledged as collateral against loans to municipalities for instance. The payments are serviced through taxes, thereby preventing us, from really OWNING property or holding our land in alodium. We pay perpetual RENT on property we THOUGHT we BOUGHT, because we insist on using I.O.U.s as MONEY.

Therefore, at all costs, we must deprive them of their land. The best means to attain this is to increase the taxes and mortgage indebtedness. These measures will keep land ownership in a state of unconditional subordination.

from 4th Protocol, Learned Elders of Zion

Private property OWNERSHIP in America is a myth, since we do not hold land in alodium, but rather must pay perpetual service

or rent

to the State (government). Failure to pay

perpetual property taxes results in seizure of the land, and in attempt to prevent such a possibility, the public must exchange its wealth for the funny money

with which to pay

the tax. But since the money

is DEBT, we CANNOT pay

anything nor are we able to discharge an obligation … unless by FIAT we can declare debts are payable with debts. And if that be so, our I.O.U.s should be just as useful to those ends as the FED's I.O.U.s. Why must we sanctify one man's I.O.U.s that are non-redeemable while we outlaw

the I.O.U.s (non-redeemable) of another? The banking system has purchased

our country with NOTES, and holds the first mortgage on us both as individuals and as a community, yet they loaned us NOthing (noTHING)!

Everyone knows what debt is when he owes it, but people sometimes forget that most of the financial assets they try to accumulate are the debts of others.

Two Faces of Debt, Fed. Res. Bank of Chicago p. 1

Even our much touted free enterprise

system is a myth, made impossible when the government decided what the parity relationship would be between gold and silver (Bi-Metalism), rather than leaving it to a free market. Certainly the government would not be expected to establish a fixed ratio of wheat to rye, potatoes to carrots, Fords to Chevrolets, etc. And the free market

concept went out the window when the Federal Reserve Act was passed (12/23/1913),establishing a PLANNED economy in which the PRIVATE BANK (FED) was in ABSOLUTE control.

Whoever controls the volume of money in any country is absolute master of all industry and commerce.

President James A. Garfield

The Federal Reserve holds the purse strings

to America, since we are a nation trying to spend

credit and the FED and their commercial banks are the source of credit. But to spend

implies payment,

and payment

implies the clearing

of a debt … but I.O.U.s CANNOT clear

DEBTS!

By creating loose money

(easy credit), the FED creates prosperity,

known to some as a boom economy.

This is done by lowering reserve requirements

(reduces the number of I.O.U.s the banks must hold in their vaults), reducing re-discount rates

(lowering the price

of new I.O.U.s the FED will sell

to the commercial banks) and repurchasing bonds

by the Federal Open Market Committee (they buy

bonds [I.O.U.s] with more I.O.U.s, thereby increasing the availability of I.O.U.s [money]. Reversing the above creates a scientifically

planned depression, recession or bust,

increasing the number of foreclosures, mergers and economic dislocations. Since a few chosen people

are given to KNOW WHEN these policy changes will come about, they HAVE TO GET RICH. It cannot be helped. The value

of stocks and commodities can be regulated,

allowing those in the know

to buy ‘em low and sell ‘em high.

The larger banking houses

such as Chase Manhattan, Manufacture Hanovers Trust, etc. are thus able to buy up large shares of multinational corporations, which in turn are busy swallowing up the smaller corporations, which in turn are soaking up the small independent businesses around the globe. Any housewife can find ample evidence of this practice by simply looking at the product labels to see who owns whom … but of course the name of the bank (which holds the mortgage to the company) is not there. But our large corporations are all swimming in that sea of debt and can be broken

by the bank at will. The power of money is awesome.

Power tends to corrupt, and absolute power corrupts absolutely.

Lord Acton

Those readers who are familiar with such organizations as the Council on Foreign Relations and the Trilateral Commission can begin to see HOW these few people have amassed such political clout. Since the inception of the CFR (incorporated in N.Y., N.Y. in 1921) and the Trilateral Commission (inc. 1973 in N.Y., N.Y.), they have retained the Chairman of the Federal Reserve Bank (of N.Y.) as a member, and were able to INCREASE their standings as a result of such scientifically created

depressions as the Panic of ‘29. Those who are not familiar with these groups should seek out a right wing extremist

for a run down

of their (CFR, etc.) goals and membership lists. These extremists

have been SCREAMING their heads off about these groups, but the press

has turned a deaf ear, perhaps the top echelons of the media are MEMBERS … (oh yes!)

These illuminated

personages are wreaking havoc with our economy, and the public is almost totally unaware of these machinations. The most recent scapegoat for our perverted monetary system

has been the Arabs. We drive smaller cars, compute gas mileage, over insulate our homes, turn down thermostats, drive slower, fly slower, trade our power boats for sailboats, build smaller homes and sell off everything we can in a flurry of yard sales and blame the Arabs for the price

of oil while our

government seizes oil rich land, places moratoriums on offshore drilling and nuclear power generation and promotes antagonism between Middle-East nations, usually in the form of pro-Israel foreign policy. Our reduced consumption of petroleum has produced a glut

of oil on the market while other people tell us we're running out of oil. The banks are still trying to convince our schoolchildren there is not enough gold for modern transactions and that now there isn’t enough oil. Any time a select few are able to corner the market in a particular commodity they invariably try to reduce the supply and boost their MARGIN. The Arabs have been made the scapegoat for our LIQUIDITY crisis. We do not have money

to buy the oil. Debt service is soaking up our funds, the paper is worthless … and the Arabs DOn’t WANT IT. Our money

is worth LESS overseas than it is here. We are the last to know! Prices are not rising

… the dollar parity

is FALLING. It takes less time to earn a dollar

now than it did a year ago, yet it takes as long (sometimes longer!) to earn a loaf of bread, or gallon of oil. Product parities are little changed from several decades ago! Only the parity of dollars

to products is changing! The problem is the MONEY.

We are absolutely without a permanent money system. When one gets a complete grasp of the picture, the tragic absurdity of our hopeless position is almost incredible, but there it is. It is the most important subject intelligent persons can investigate and reflect upon. It is so important that our present civilization may collapse unless it becomes widely understood and the defects remedied very soon.

Robert Hemphill, Federal Reserve Bank of Atlanta, Ga.

The United States began a MONETARY COLLAPSE in 1933 when the gold window was shut to American depositors. The collapse was completed when in 1968, the silver window was closed to Americans and an entirely NEW system replaced CASH. FIAT money

put America on 100% CREDIT, and the debts began to accelerate as we left cash and credit behind us. Since 1968, the United States has been without a money of account.

We are pouring walls MEASURED in cubic yards … but we do not have the CONCRETE! Only a fool would build on that foundation. Perhaps this explains our lack of zeal and ambition; maybe we know somehow we are on the treadmill to oblivion.

Mortgage payments on homes are running 30 to 40 years! The owner

will be upwards of 70 years old by the time the last payment rolls around, but he may be forced out of his own

home by mandatory retirement, leaving him DEPENDENT upon government for housing. We could understand these things if they happened in Russia, but this was once the land of opportunity

! Foreclosure is a FACT!

Take a ride across this nation and take a good look at us. We have the best growing climate of any large nation in the world, and our land is still suitable for producing food. We FEED most of the free world and not satisfied with that, we pump foodstuffs into Communist countries to boot! There is more than enough room for us, we have more than enough natural resources to house us, clothe us and make us comfortable; we have more resources than we honestly know what to do with. We even acknowledge ourselves as WASTEFUL! And to salve our conscience, we even GIVE OUR WEALTH AWAY … a practice that is UNPRECEDENTED in HISTORY. We SUPPLY OUR ENEMIES! ! ! We are INDEPENDENTLY WEALTHY! Yet we have the most horrific DEBTS ever amassed by a single nation and have no hope of ever paying them off. It cannot be done. We are being forced off our OWN land because we BELIEVE the money

is WEALTH … when the bankers got it for NOTHING. So deluded have we become, that we often ignore the implications of such statements as these (appearing in The National Debt, FED Bank of Philadelphia):

A large and growing number of analysts, on the other hand, now regard the National Debt as something useful, if not an actual blessing.

… the impact and effect of the Debt depends on who puts up the money and how they do it.

… the identity of the lenders is the key. (how about WHAT they lend — BGM)

When a bank buys Government securities, it creates new checkbook money. (Wow! Can we do that? — BGM)

… the Federal Reserve buys Government securities and pays out a special money the banks can use as reserves to increase their lending capacity.

Bankruptcy, in simplest terms, occurs when lenders demand repayment and the borrower can’t make it. What are the chances that a significant proportion of the lenders of the National Debt will demand repayment? Very slight.

… most lenders would rather keep the securities than get their money back.

The Federal Government, with the cooperation of the Federal Reserve, has the inherent power to create money — almost any amount of it. (!!!!) This power makes technical bankruptcy out of the question. Yet this power also makes it possible for Governments to pursue policies that could have even more disastrous results than bankruptcy. (!!!!)

Debt has a deceptive, something-for-nothing kind of charm.

Used recklessly, it has the power to make us its slave.

This country, and indeed the countries of the world, are in deep trouble, but the money lords

continue to shower us with calming phrases and tender words for fear of truth is their only qualm.

Every kind of loan proves infirmity in the State … Foreign loans are leeches which there is no possibility of removing from the body of the State until they fall off of themselves or the State flings them off. But the goyim [non-Jewish] States do not tear them off; they go on persisting in putting more on to themselves so that they must inevitably perish, drained by voluntary bloodletting.

from 20th Protocol

The prosperity is over, Our liquidity has vanished, leaving in its wake astronomical debts, bankruptcies, vacant shops, unemployment and hardships … but the worst is yet to come. This tragic course is destined to wipe out savings, retirement pensions, social security

and most of all, the PRODUCER of WEALTH. The American farmer is locked in a death struggle brought about by debt expansion, and unless we abandon debt money,

we may soon see mass starvation in the country which once fed the world. We are on a course leading, to more disastrous results Ian bankruptcy

! Possibly a worldwide collapse of trade … and what will the cityfolks

do without food PRODUCED by the LABOR of countryfolk

?

Are there FOOLS enough to think our GOVERNMENT has resources

to cope with our problems? Governments HAVE NO RESOURCES but what WE GIVE THEM or THEY TAKE FROM US! ! ! And that is precisely the purpose of monetized debt,

to take from the PRODUCER and administer to the weakling, garnering his popular support for PROGRAMS and HANDOUTS that are made POSSIBLE by PRODUCERS … not money. The money is the TOOL of expropriation.

But history teaches us that we learn nothing from history (because it is not TAUGHT … another interesting subject, but beyond the scope of this text) and we appear doomed to repeat the mistakes of others. The French Revolutions (they had three interrelated ones beginning in 1789) and the Bolshevik Revolution (1917) in Russia both accompanied currency instability

and starvation, resulting in the deaths of some 18 million Russians during their agricultural reforms

as Big Brother began to PLAN the economy in violation of natural law. Our gasoline allocation plan

of the ‘70s should serve to remind us of government ineptitude in solving

problems.

A planned economy does not work. Such a system becomes fraught with bureaucratic nightmares involving over-regulation, controls, de-controls, police state methods of enforcement, violation of property rights, civil rights, shortages, surpluses, and always the hidden forces of monopolies. In fact, so many problems did Lenin, and later Stalin, have, that concessions

(fancy word for monopolies) were granted to American firms as early as the 1920s, in an attempt to bail out

Communism. And our companies (e.g. Westinghouse, Ford, Standard Oil, RCA, etc.) began to exploit Soviet Russia in an atmosphere of NO COMPETITION. Who could ask for a better deal?

The Most grandiose Bolshevik achievements of the thirties, which glorified communism throughout the world and convinced two generations of American and European intellectuals of the economic potency of the U.S.S.R. and of central planning, were all achievements of Western capitalism.

William E. Simon (A Time for Truth), former Secretary of the Treasury.

Freedom in America spawned the FREEMAN of the West who owned his own home and the things in it, and was beholden to no man, but rather acknowledged that God had given us the things of this earth. However, we were easily tempted to want more and more, paying later and later, all the while coveting money

which soon became debt.

We have exceeded the bounds of natural law and now reap the curse outlined in the 'Book of books.

The stranger who is within thee shall get up above thee very high, and thou shalt come down very low. He shall lend to thee, and thou shalt not lend to him; he shall be the head, and thou shalt be the tail.

Deut. 28:43, 44

Money is a reflection of the people who use it. A sound money (wealth) reflects the image of a thrifty, hard working and industrious people who pay their obligations and honor their commitments. A sound money SETTLES debts ON THE SPOT because it is tangible evidence of WORK ALREADY ACCOMPLISHED. Sound money can be saved without fear of devaluation, because nobody can COUNTERFEIT production. Sound money does not have to keep working

in a futile attempt to keep pace with inflation.

A sound money is an ACCOMPLISHED FACT, not a hollow promise to gladly pay you Tuesday.

A sound money reflects common sense principals that are so simple as to be overlooked by our educated

populous. That is, the larger (heavier) the coin (of silver or gold), the more it is worth. That almost seems dumb, but just ask yourself why a copper penny is worth only 1 cent when it has more metal than a dime composed of mostly copper (and some nickel). Why should a 5 cent piece be worth half as much as a dime when the dime contains a cheaper substance?

How can a Susan B. Agony

coin be worth 400% of a quarter when it only contains 50% more of the same metals?! Would we pay four (4) times more for a 1 ½ lb. steak than a 1 pound steak? When does TRUST become GULLIBILITY?

Through guarantees that a paper money could be exchanged for something of intrinsic value, gold served to inspire a measure of confidence in the system. Without the confidence factor, many believed a

Gold, Federal Reserve Bank of Philadelphiapaper moneysystem is liable to collapse eventually. Present experience suggests … that the only confidence required is a firm conviction that money will be accepted as payment for goods and services. The issues are economic, political and even psychological.

How do we stack up today? Are we thrifty, or spendTHRIFTS? Are we FREE of personal debts or are we INTERDEPENDENT as a result of high mortgages and loans? Is our money a good storehouse of value, or do we seek high interest yields

that CANNOT keep pace with REAL cost increases. Who is fooling whom? The FED knows the paper is no good, otherwise they would give us something for it. The Treasury knows the paper is no good, otherwise they too would give us something for it. WE ARE THE LAST TO KNOW. The only reason we continue to take the stuff

is because there are still a lot of suckers who don’t KNOW the cupboard is bare.

Of all the contrivances devised for cheating the laboring classes of mankind, none has been more effective than that which deludes him with paper money.

Daniel Webster

Free Enterprise gave way (in the 19th Century) to CAPITALISM. And the consolidation of multinational corporations has been effected by those who control CREDIT. And the eventual result will be MONOPOLIES controlled by the BIGGEST of monopolies, the Federal Reserve and their co-conspirators the Commercial Banks! As a worldwide movement this can be seen as Communism … a system of totalitarian control brought about through the control of a nation's credit.

The Bankers own the earth. Take it away from them, but leave them the power to create deposits, and with the flick of the pen they will create enough deposits to buy it back again. However, take it away from them and all the great fortunes like mine will disappear, and they ought to disappear, for this would be a happier and better world to live in. But if you wish to remain the slaves of Bankers, and pay the cost of your own slavery, let them continue to create deposits.

Sir Josiah Stamp (former President of the Bank of England)

Our government is nothing more than a front

corporation being used by personages behind the scenes

to control and enslave us while keeping up the PRETEXT of freedom through phony elections and slogans of brotherhood, equality and freedom.

Every candidate since Roosevelt (FDR) has been a member of the CFR or Trilateral Commission … they CANNOT lose when they load the dice! In this last election (1980), they had as members: George Bush (Trilateral), John Anderson (Trilateral) and Jimmy Carter (co-founder of Trilateral Commission). The founder

of the T.C. was David Rockefeller, and the founder

of the CFR was John D. Rockefeller (along with Paul M. Warburg, Chairman of Federal Reserve in 1921).

We are stimulated to spend, then forced to curtail; our land is zoned and restricted and we obtain permits to paint our house a different color and flush the john! Our land use is regulated and our cities are urban renewed;

some prices are controlled while others are subsidized. We are stifled by taxes that penalize improvements for us, then we're prodded to improve

by write-offs and tax credits. All of us chase the exemption and allowance

carrots and can’t wait to engage the services

of tax experts

who never figured out (nor wanted to) that WE DOn’t FINANCE OUR GOVERNMENTS ANYWAY!!!! Meanwhile, the enlightened ones

continue to poke us in the face to make us slow down and kick us in the ass to make us speed up! No wonder America suffers from mental trauma and upset stomach. Our government agencies are loaded down with smug, self-serving bureaucrats who feel no compunction to OBEY THE LAW. They took away our MONEY OF ACCOUNT (silver and gold) and insist now (so do the bankers!) that DOLLARS are BOTH THE MONEY and the MEASURE OF IT! But the UNIT of the money CANNOT be the MONEY too!

Our representatives must be made aware of the LAW that SOMETHING must be the MONEY for which the DOLLAR is the UNIT OF MEASURE. We must REPEAL the LEGAL TENDER ACTS, without which Gresham's Law would collapse as so much hot air. Nobody would take PAPER (non-redeemable) when they could take GOLD AND SILVER. Only when legal tender acts FORCE the use of bad money

does Gresham’s law work, and drive out the good money.

We must ABOLISH the Federal Reserve and EXPUNGE the debts owed to those who CREATED (out of nothing) the money

to obtain Government securities. The money is IMAGINARY, and so are the DEBTS. This ILLUSION must stop. We must ABOLISH fractional reserve banking which permits multiplication of deposits,

thereby creating something that does not exist. We must return to FREE COINAGE of gold and silver of a known weight and fineness, not expressed in dollars

which is a term expressing just another unit of measure (either the grain or troy oz.), and we must stop voting for debt producing bond issues which continue to burden us with ever increasing interest on loans of nothing tangible.

Credit, you see, is a

Keeping Our Money Healthy, Federal Reserve Bank of N.Y.productthat is bought and sold.

Credit does not EXIST as a tangible thing, cannot be seen, weighed, touched, smelled or heard. So how is it that one person (a banker) is given the EXCLUSIVE privilege to create (invent) units of nothing and loan them out at interest to all manner of individuals who do not have this power

? And if they loan us credit

why don’t we just invent some credit

of our own and REPAY THE BANK IN KIND. Maybe we can use the book of Genesis as our authority. The expression used was: Kind after its kind.

Or we can rely upon the Federal Reserve for sound reasoning.

Money is any generally accepted medium of exchange, not simply coin and paper currency. Money doesn’t have to be intrinsically valuable, be issued by a government or be in any special form.

I Bet You Thought, Federal Reserve Bank of N.Y.

The Federal Reserve tells us (in their wonderful books) that demand deposits are money, bank liabilities are money, Federal Reserve Notes are liabilities of the FED, and are money, debts are assets, and no telling what else might be money … imagination is a wonderful gift!

Yet -

Money: In usual and ordinary acceptation means coin and paper currency used as circulating medium of exchange, and does NOT EMBRACE NOTES, BONDS, EVIDENCES OF DEBT …

Lane v. Railey, 280 Ky. 319,133 S.W. 2nd 74,79,81

But —

The Federal Reserve System works only with credit.

Keeping Our Money Healthy

And credit is a correlative of a debt and means:

… the right granted by a creditor to a debtor to defer payment of debt or to incur debt and defer its payment.

Uniform Commercial Credit Code, Section 1.301(7)

And — if the system uses only CREDIT, which is the DEFERMENT OF PAYMENT, WHAT will we use to PAY our debts once we decide to stop DEFERRING them?

Money by itself is really useless. But as a medium of exchange it has value. And that value is what money can buy — its purchasing power.

Keeping Our Money Healthy

Let's analyze the first sentence. Is money

by itself really useless? Wouldn’t that depend on WHAT was being used AS money? Cows were once used as money, yet their milk, cream, butter, meat and hides were useful. Tea has been used as money, and there are many folks who enjoy a hot (or iced) tea beverage as a refreshing stimulant. Salt was used as money, and was used extensively to cure and preserve meats as well as enhance the flavor of foods. Nothing useless about that. Tobacco was once used as money in the U.S., and while this writer doesn’t smoke, there are those who derive some satisfaction from tobacco. Iron was used as money, and could be melted down and used for hinges, cannonballs or even shipbuilding. Silver has been used as money, and could be melted down to make jewelry, filling material for cavities in teeth, even used in the electronics industry, along with copper and other metals. Gold is useful for ornaments, gold leaf lettering, rings, etc. having outstanding properties not possessed by any other material. Everything that has been used AS money (strictly construed) has been useful and recognized as most swap-able

in the region of general use. So how can the FED say that money is useless by itself? Because we aren’t using anything as money, and there is no such THING, in and of itself that is money. Our money exists only in the imagination.

The words value

and worth

express intangibles and are grossly misused. What is a refrigerator worth

to an Eskimo? How much would it be worth

to a butcher in Atlanta in August? What value

would a housewife put on a guided missile? Or a transponder? Might a pilot value

these things more highly? So if value

is an intangible with no FIXED form of expression, how can there be UNITS (all equal) of an UNMEASURABLE? Value

is the desire or human satisfaction that is realized by the use or acquisition of a product or service.

Strange, isn’t it? One dollar always has equaled 4 quarters or 10 dimes or 20 nickels or 100 pennies. The dollar itself doesn’t change. But what the dollar will buy, how much it will buy, does vary.

Keeping Our Money Healthy

Nothing at all strange about the equation! The dollar doesn’t change because it is a unit of measure, and the unit of measure has not changed. What has changed is what they are trying to measure WITH it. If a fisherman customarily exchanged 100 pounds of whole haddock for 200 pounds of Maine potatoes, what might he expect to buy with 100 pounds of haddock bones? There isn’t a farmer dumb enough to let the fisherman eat the meat off the haddock and tender the bones for the potatoes and expect the same parity to exist. So how is it the American (and other) people are so foolish as to accept a quantity of copper (with a little nickel finish to make it look like silver) and still think of it as real money? It took a long time to make us this dumb, but the school systems have done an admirable job for their masters. When the Rockefeller Foundations (along with Carnegie) supply over 50% of the funds for the top 20 teacher's colleges (in this century), then we get an idea of WHO decides WHAT will (or will not) be taught. It is NOT left to the PARENTS! The BANKS run this country and everything in it. And some banks are more powerful than others. David Rockefeller who controls Chase Manhattan and First National City Bank ( of N.Y.) controls (with 10% or more stock) the top 23 industrials, the top 9 in transportations and the top 3 insurance companies in the U.S., not counting foreign holdings. The United Nations sits atop Rockefeller donated land, and they have a full time personal envoy to the U.N. … they are a NATION unto themselves. Yet they are rated as subsidiary to the Rothchild family of Europe.

The Bureau of Engraving and Printing in Washington, D.C., a unit of the Treasury, is responsible for printing the nation's currency. BUT ITS ORDERS TO PRINT COME FROM THE 12 FEDERAL RESERVE BANKS, not the President or Congress. THE RESERVE BANKS, NOT THE TREASURY, DETERMINE HOW MUCH CURRENCY IS PRINTED …

I Bet You Thought, Federal Reserve Bank of N.Y., which is located across the street from Chase Manhattan Bank. (emphasis mine)

The 12 regional Reserve Banks AREn’t GOVERNMENT INSTITUTIONS but CORPORATIONS NOMINALLY

(from I Bet You Thought)OWNEDBY MEMBER COMMERCIAL BANKS.

If the government doesn’t own them, and the member banks don’t own them … WHO DOES? Could it be that a powerful family (European) that has gained control of the Bank of England (a Private corporation), the Reichsbank of Germany (ditto) and the central bank of the Soviet Union (resulting from N.Y. and London support